![]()

Before the Federal Communications Commission

In the Matter of Customer Proprietary Network Information

CC Docket No. 96-115

To: The Commission:

Comments ofThe Electronic Privacy Information Center, Consumer Action, Privacy Rights Now Coalition, Center for Digital Democracy, Consumer Federation of America, Privacy Journal, Center for Financial Privacy and Human Rights, and National Consumers League on the Petition for Rulemaking to Enhance Security and Authentication Standards for Access to Customer Proprietary Network Information

April 14, 2006

Pursuant to the notice published by the Federal Communications Commission concerning Customer Proprietary Network Information,[1] the Electronic Privacy Information Center, Consumer Action, Privacy Rights Now Coalition, Center for Digital Democracy, Consumer Federation of America, Privacy Journal, Center for Financial Privacy and Human Rights, and National Consumers League submit the following comments.

The Electronic Privacy Information Center (EPIC) is a public interest research center in Washington, D.C. It was established in 1994 to focus public attention on emerging civil liberties issues and to protect privacy, the First Amendment, and constitutional values.� In 2005, EPIC filed a petition seeking enhanced protections for CPNI.[2]

Consumer Action is a non-profit, membership-based organization that was founded in San Francisco in 1971. During its more than three decades, Consumer Action has continued to serve consumers nationwide by advancing consumer rights, referring consumers to complaint-handling agencies through our free hotline, publishing educational materials in Chinese, English, Korean, Spanish, Vietnamese and other languages, advocating for consumers in the media and before lawmakers, and comparing prices on credit cards, bank accounts and long distance services.

The Privacy Rights Now Coalition was organized by Ralph Nader and Remar Sutton to highlight the efforts of the key non-profit organizations that care about the integrity of your private life.

The Center for Digital Democracy is committed to preserving the openness and diversity of the Internet in the broadband era, and to realizing the full potential of digital communications through the development and encouragement of noncommercial, public interest programming.

Since 1968, the Consumer Federation of America (CFA) has provided consumers a well-reasoned and articulate voice in decisions that affect their lives. Day in and out, CFA's professional staff gathers facts, analyzes issues, and disseminates information to the public, policymakers, and rest of the consumer movement.

Privacy Journal is the most authoritative publication in the world on the individual's right to privacy.� Its publisher is Robert Ellis Smith, who is recognized as the leading expert on the right to privacy in the U.S. He is an experienced journalist, a lawyer, an author of several essential books on privacy. Twice he has been asked to write the definition of privacy for the World Book Encyclopedia.

The Center for Financial Privacy and Human Rights, a non-governmental advocacy and research organization, was founded in 2005 to defend privacy, civil liberties and market economics. The Center is the only non-profit human rights and civil liberties organization whose core mission recognizes traditional economic rights as a necessary foundation for a broad understanding of human rights.

National Consumers League's mission is to protect and promote social and economic justice for consumers and workers in the United States and abroad. The National Consumers League is a private, nonprofit advocacy group representing consumers on marketplace and workplace issues. It is the nation's oldest consumer organization.

The EPIC Petition and Related Pretexting Developments

In July 2005, EPIC filed a complaint with the Federal Trade Commission concerning a website that offered phone records and the identities of P.O. Box owners for a fee through pretexting.� Pretexting is a practice where an individual impersonates another person, employs false pretenses, or otherwise uses trickery to obtain records.��

The owners of the California-based business operating the website responded to the EPIC complaint, claiming that they knew of no law that prohibited them from selling phone records!� Other pretexters have taken the same approach.� They have ignored general consumer protection norms and argued that no specific law prohibits pretexting.

EPIC supplemented the July filing in August with a list of 40 websites that offered to sell phone records to anyone online.� In light of the fact that so many companies were selling communication records online, EPIC also petitioned the Federal Communications Commission, urging the agency to require enhanced security precautions for phone companies� customer records.� Although telephone carriers unanimously opposed enhanced security requirements, proposing that lawsuits against pretexters would solve the problem, the FCC unanimously granted the petition and is seeking comments on enhanced security standards for phone records.

Most recently, EPIC wrote to the American Bar Association and 50 states' bar ethics committees to explain that attorneys are hiring investigators and online data brokers to pretext.� EPIC argued that it is unethical for attorneys to employ these practices, and urged the state authorities to advise attorneys not to buy pretexting services.

We continue to believe that action is needed at the federal and state level to protect this information.� Phone records can be used by individuals to stalk and harass other people.� They can be used for corporate espionage purposes.� While some claim that pretexting is a legitimate research tool, that argument is mere sophistry.� Those who have a legitimate need for phone records can obtain a court order in order to access the information.� Pretexting is simply an end-run around existing legal access provisions for people who probably do not have a legitimate reason to obtain calling data.

An archive of EPIC's efforts is available online at http://epic.org/privacy/iei/

Specific Comments

11. Pursuant to our authority under section 222 of the Act, we seek comment on the nature and scope of the problem identified by EPIC.

Many different records are offered for sale on websites.� These include wireless and wireline phone records, the calling name associated with a phone number, the location of the phone user, information associated with communications-linked navigation services, such as GM Onstar, and the identities associated with interactive computer services.� Outside the telecommunications field, these sites are offering asset searches (where the investigator calls banks and determines how much money the victim has in accounts) and Social Security Numbers.

Each of these records may have different sources.� But most indications are that phone records information is being obtained directly from carriers.�

However, calling name information may be obtained from a carrier, or perhaps from one of the industry-operated Caller ID databases such as CNAM.�� There is also the possibility that data brokers are selling calling name information from databases derived from Automatic Number Identification.� Several companies, including Intellius.com, advertise "ANI" generated databases.� It is unclear whether these databases comply with Commission rules at 47 CFR 64.1601.� An advertisement for Intellius.com's "Reverse ANI" databases appears below.

Location data may be obtained from carriers, but we are also aware of location services where the investigator simply calls the victim and asks "where are you?" or engages in some artifice to trick the victim into revealing location ("you've won a prize from the local radio station, tell us where you are so that we can bring it to you").�

Increasingly-popular automobile navigation products, such as GM's Onstar, can provide vehicle location information.� This information is obtained directly from the Onstar service through pretexting.

Abika.com has offered information concerning the identities of users of AOL and several dating services, such as Match.com.� In these searches, the purchaser provides an AOL screenname or Match.com "handle" which is then linked to a real identity by Abika.� While it is possible that this information could be discovered through web searches, we believe that the service providers themselves are targeted to obtain information.�

We believe that these different types of records are obtained in three different ways: pretexting, computer intrusion, or through insiders.� Each one of these threats has to be addressed in different ways.�

In order to address pretexting, the process of the practice must be clearly understood.� We think that in the typical pretext, the pretexter obtains a telephone number of the victim from the person seeking phone records.� The pretexter then uses a personal information database to buy identifying information on the victim, including mother's maiden name, date of birth, address, and Social Security number.� With this biographical information, the pretexter then calls the carrier, pretending either to be the victim, or pretends to have the authority to access the victim's records.� Carriers often authenticate customers by simply asking their name, billing address, and last four digits of the Social Security number.� If successful, the pretexter is sent the records, and they are passed on to the person seeking the records.� Critical to the success of pretexting is carriers' reliance on widely-available personal identifiers to authenticate customers.� We will expand on this problem later in the comments.

Computer intrusion and insiders present a separate set of problems.� These are best addressed through auditing of access, better design of online billing systems (for instance, not assigning an easy-to-guess default password), and through enforcement actions.�

12. We also seek comment on whether our existing opt-out regime sufficiently protects the privacy of CPNI in the context of CPNI disclosed to telecommunications carriers� joint venture partners and independent contractors�

Information sharing can exacerbate privacy risks.� Information sharing can be used to target market individuals for fraudulent products and enable other types of fraud.� The more information is shared, the greater the risk that is may be acquired by dishonest employees or others who have access to data in the course of its transfer.� There is increasing evidence that insiders who have access to personal data present serious risks for identity theft and other fraud.� A news report covering a study from the Michigan State University indicated that a researcher found in a review of 1,000 identity theft cases that between 50-70 percent were insider jobs:

[The] director of an identity theft program at Michigan State, randomly selected 1,037 cases from around the country, then painstakingly traced each incident to its origins. In 50 percent of the cases, the victim's identity was originally pilfered by a company employee. In another 20 percent of cases, evidence strongly suggested dirty play by an insider.[3]

In the financial services industry, insider risks are so severe that the Office of the Comptroller of the Currency has warned banks that organized crime rings were placing low-level employees in financial institutions to commit fraud.� In an April 2002 security alert, the agency warned:

�[I]ndividuals are being encouraged by gang members to apply for teller positions at financial institutions for the sole purpose of providing access to the institution's operating systems and customer access information.[4]

Only recently has the frequency of security breaches into databases containing sensitive personal information come to light.� The frequency of security breaches at leading financial institutions and elsewhere suggests that information sharing among affiliates can increase the likelihood of consumer harm.� These security breaches can readily result in fraud on the consumer.� Consumers, therefore, are legitimately concerned that the greater number of affiliates accessing their information, the greater the possibility that it will be revealed to others.

There is substantial independent evidence verifying that an opt-in approach is the only effective method to protect sensitive private information. An opt-out approach is inadequate because it is not calculated to reasonably inform consumers about their privacy options. Not only is the burden on the customer to return their opt-out notice, such notices are vague, incoherent, and often concealed in a pile of less important notices mailed in the same envelope from the same source.[5] The importance of the notices, as well as their purpose, is rarely brought to the customer's attention in any coherent fashion. Studies have revealed, "the majority of the general public is still unaware of the exact nature of marketing uses and the availability of opt-out choices."[6]

When it is in the economic interest of a company to prevent a consumer from taking a certain action, companies tend to erect barriers to consumer choice.� Opt-out is the standard choice for companies that are trying to stop consumers from taking an action.� For instance, the Wall Street Journal reported on barriers to consumer choice in 2003, noting that some industries had resorted to opt-out style automatic renewal policies:

Breaking up is getting harder to do.

From AOL to EchoStar, a growing number of U.S. companies are coming under fire from regulators who claim they are deliberately thwarting customers' efforts to cancel their service contracts.

[�]

�magazine-industry sales tactics are drawing the attention of regulators. To fight churn, many publishers, including Time Inc., are switching to a "self renewing" subscription model, which means the publisher automatically charges subscribers' credit cards for another year, unless customers proactively cancel their subscriptions. At Time Inc., about 20% of subscriptions, including many popular titles such as Sports Illustrated, Fortune and Money, are sold on this continuous subscription model�[7]

In the case of data broker Acxiom, the company refuses to accept "third-party opt-out requests."� These requests are generated by privacy-enhancing businesses that opt out clients in bulk from marketing lists.� Acxiom rejects these opt-out requests because the company wants to provide the individual concerned a privacy policy first and hear from the individual directly.[8]

For more perspective on this problem, it is worth revisiting Ting v. AT&T, 182 F. Supp. 2d 902 (2002). In that case, AT&T developed a new standard customer contract that contained an arbitration clause in order to remove consumer disputes from court. In developing this new consumer contract that reduced consumers' rights, AT&T did research to determine how to present it so that customers wouldn't read it or take action to opt-out of the new contract. The trial court noted that the AT&T research found:

In the letter it should be made clear that this agreement is being sent for informational purposes only. The fact that no action is required on the part of the customer needs to be made. A strong link establishing that this information is not a "call to action" on the part of the customer should be clearly stated in the letter...Customers should understand that the mailing is being sent to comply with a federal mandate and does not imply any change in their relationship with AT&T.

In sum, there are dozens of ways that an opt-out framework can be designed to limit consumer choice.� An opt-in framework would better protect individuals' rights, and is consistent with most United States privacy laws.� For instance, the Family Educational Rights and Privacy Act, Cable Communications Policy Act, Electronic Communications Privacy Act, Video Privacy Protection Act, Driver's Privacy Protection Act, and Children's Online Privacy Protection Act all empower the individual by specifying that affirmative consent is needed before information is employed for secondary purposes.[9]

Further, public opinion clearly supports an opt-in system for information collection and sharing.� A study conducted by the American Society of Newspaper Editors (ASNE) and the First Amendment Center (FAC) in April 2001 illustrated strong support for privacy and specifically for opt-in systems.[10]� In that study, the respondents indicated that personal privacy was an issue as important as crime, access to health care, and the future of the Social Security system.

In other information collection contexts, individuals regularly indicate that opt-in is preferable to opt-out.� The ASNE/FAC study shows that 76% of individuals support opt-in as a standard for sharing of driver's license information.� A study conducted by Forrester Research found that 90% of Internet users want the right to control how their personal information is used after it is collected.[11]� A study conducted by the Pew Internet and American Life Project found that 86% of Internet users favor opt-in privacy policies.[12]� And, a BusinessWeek/Harris poll in 2000 found that 86% favored opt-in over opt-out.� The same poll showed that if given a choice, 90% of Internet users would either always or sometimes opt out of information collection.[13]

This popular support for opt-in manifests itself when consumers are actually given the opportunity to vote on matters of privacy.� In a ballot referendum, voters in North Dakota favored requiring financial institutions to obtain the affirmative consent (opt-in) of consumers before sharing information with third parties over opt-out, which was favored by the Legislature and banks.� Although proponents of stronger privacy protections were outspent by seven to one,[14] the North Dakota financial privacy initiative passed with the support of 73% of the voters.[15]

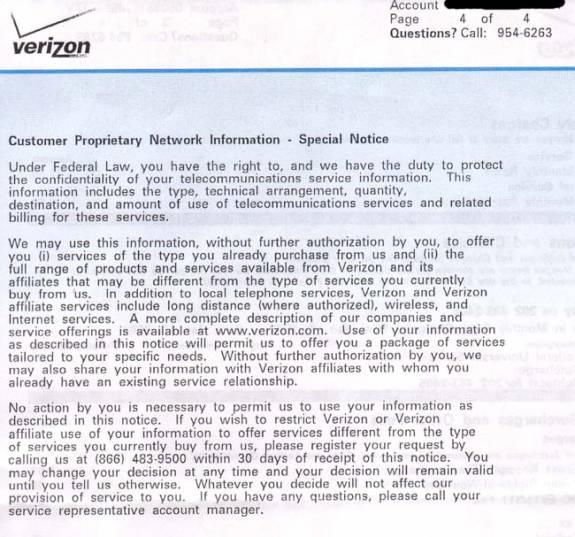

Phone companies have thwarted opt-out processes by demanding excessive authentication for opting out.� For instance, the opt-out process for Customer Proprietary Network Information (CPNI) data sharing established by Verizon was confusing, and placed the burden on individuals to navigate a five-step process in order to opt-out.[16]� In addition, the Verizon CPNI notice appears on the back side of the last page of the bill.� It does not even mention the word "privacy."[17]

Verizon's and other carriers' CPNI opt out procedures differ from state to state, or region to region.� As a result, there is no coherent way for consumer advocates to provide simple information to help consumers navigate the opt-out process.� Oddly enough, the same companies that say they need national, uniform regulations impose upon consumers widely-varying procedures to protect privacy.

The most comprehensive effort to provide information on opting out of CPNI was performed by the Privacy Rights Clearinghouse.� Because of the differing practices, at the time that survey was completed, many regions were not covered.� Furthermore, the survey showed that many carriers did not have any mechanism to perform online opt outs.[18]

Finally, EPIC has received many complaints from consumers that they have called carriers to request to opt out, but the customer service representatives do not know how to handle the calls.[19]�

Carriers are likely to argue that an opt-in regime will violate their First Amendment rights of commercial speech.� They will cite to a single case--U.S. West v. FCC--for this proposition.[20]� Since that case was decided, every major challenge to privacy law based on commercial free speech has failed.[21]� The FCC should reevaluate the strength of the U.S. West argument in light of the fact that most attempts to create expansive substantive due process rights for information sale have failed.

We believe that U.S. West was an anomaly.� In fact, even in the challenge to the Do-Not-Call Registry, which was brought in the 10th Circuit to leverage the U.S. West precedent, the court upheld the Registry without even citing to U.S. West.[22]�

16. We solicit comment on the advisability of requiring carriers to adopt a consumer-set password system to protect access to CPNI. Would requiring the use of passwords materially increase the security of CPNI?

Passwords would materially increase the security of CPNI, because the current reliance on biographical information is no longer sustainable.� Biographical information is easily obtainable by pretexters.� Dozens of websites advertise the availability of Social Security numbers, dates of birth, and mother's maiden names--the currently-used authentication tools by many carriers.� Public records also contain many biographical identifiers.� Investigators have subscriptions to "commercial data broker" services where biographical identifiers can be purchased for under $5.� And finally, jealous lovers--major purchasers of phone records--have all the information the need to pretext their spouse or significant other.

With the widespread availability of these biographical identifiers, it is becoming impossible to condition access to information based on possessing them.

We acknowledge that passwords are not a perfect solution to accessing records.� No single approach is likely to address all situations and threats in a security system.� However, some sort of non-biographical password system can reduce the risk that records are disclosed.� Elsewhere, we have suggested "shared secret" password systems.� This approach uses non-sensitive information that unlike biographical identifiers, does not usually appear in a database.� Under this approach, the customer would be asked several questions when they sign up for service.� Examples include:

What was the name of your first pet?What was the name of your elementary/high school?What is your favorite color?What is the middle name of your brother/sister/friend?Etc.

This information is not likely to be found in databases operated by commercial data brokers, and thus is not available to pretexters.

17. Audit trails. EPIC suggests that we require carriers to record all instances when customer�s records have been accessed, whether information was disclosed, and to whom.

We renew our call for auditing of customer access to CPNI.� Current regulation already requires such auditing when CPNI are used for marketing purposes.� Expanding this requirement to consumer access should not create unreasonable burdens.

Maintaining an audit log also makes it possible to search for anonymous access (or attempted access) patterns.� For instance, multiple attempts to obtain the same record over a short period of time may justify investigation.� Audit logs also make it possible for carriers to routinely investigate disclosures to see whether they are legitimate after the fact.� For instance, the carrier could take a sample of 1,000 record releases and investigate them in detail to determine whether pretexting was actually involved.

Effective auditing should go beyond recording access to a specific customer's record.� Abnormal access to consumer records should cause red flags to be raised.� For instance, if in a normal day, a customer service representative accesses 50 accounts, there should be detection systems in place to address situations where certain employees access greater numbers of accounts.� Employees who are accessing greater numbers of accounts may be engaging in fraud.� For instance, the Wall Street Journal recently reported on a case where bank employees sold the information of 500,000 account holders:

Experts say the breach could have been avoided if the banks had detected abnormal activities on their computer systems early on. The employees involved would normally have accessed 30 to 40 customer records in a normal business day, according to police. As the theft occurred the employees were sometimes accessing 300 to 400 customer records a day -- an anomaly that could have been spotted had the right protections been in place.[23]

In addition, in a pretexting lawsuit brought by Florida Attorney General Charlie Crist, phone logs show that Global Information Systems called a single carrier 5,100 times in a single month.[24]� So many calls from a single source should raise red flags.� Carriers should have systems in place to not only record ANI or CID, but also to detect suspicious patterns of access.�

21. Notice. EPIC suggests that companies notify customers when the security of their CPNI may have been breached.

We wish to inform the Commission that existing state security breach notification laws may not be triggered when records are obtained through pretexting.� Security breach notification laws generally are triggered where there is unauthorized access to a Social Security number, driver's license number, or financial account number and PIN.� When a pretexter calls a carrier to obtain a victim's records, there may not be unauthorized access at the carrier to one of these three identifiers.� That is, the pretexter probably already has the Social Security number when he calls, and in most cases, it probably not given access to the carrier's database with the three covered identifiers.� Therefore, in many cases, state security breach notification law will not be triggered by a successful pretexting event.

We continue to believe that carriers should give notice where there are security breaches or attempts to pretext a certain account (many pretexters make several attempts to get data before they are successful).� Notice to the subscriber could allow individuals to take actions to avoid stalking or domestic violence.� Notice will also allow individuals to pursue private claims against the pretexter or person employing the pretexter.

22. We invite commenters to consider the potential value of notification as a precautionary measure before releasing CPNI. For example, we seek comment on whether carriers should be required to call the customer�s registered telephone number for that account to verify the customer�s identity before releasing CPNI to that subscriber. Should certain types of requests trigger an advance notification requirement?

Notification in advance of releasing CPNI could thwart many pretexting attempts.� We believe that in most cases, the pretexter does not have possession of the phone for which records are sought. Therefore, sending a SMS to a wireless phone, initiating a call to the phone, or even leaving an automated voicemail on the phone account may tip the victim off to the invasion of privacy.��

24. Public response to EPIC�s petition reflects concern that improper release of CPNI can have dire consequences for customers� personal safety. Should we require carriers to permit customers to put an absolute �no release� order on their CPNI, possibly subject to existing exceptions in section 222(c)(1)?63

We believe individuals should be able to specify that their records should not be released at all, or that the release should only be to the billing address on file.

The Commission should also evaluate the protections for subscriber information.� This information, which may reveal a home address and other personal data, is sensitive.� Many people do not want their address information sold or disclosed to others (this can include domestic violence victims, judges, stalking victims, police officers, the mature, minors, etc.).� There should be an ability to restrict the dissemination of this data, regardless of whether one is a member of some class that is vulnerable to criminals, staking, or consumer scams.

25. Other approaches. We encourage commenters to think broadly and creatively about how best to guard against fraudulent or unauthorized disclosure of CPNI.

There are myriad approaches to securing data, and new technologies may bring innovative approaches to the problem.� We suggest that the Commission's rules give carriers flexibility to implement new security approaches.� We also suggest that the Commission routinely revisit security issues on a planned schedule (for instance, every 5 to 7 years) to account for new technological approaches.

27. Reporting and Notification. In part because �CPNI� is not a term with which most customers are familiar, we seek comment on whether the notifications carriers provide subscribers regarding the use and disclosure of CPNI are written clearly enough so that customers adequately understand that the notices concern the privacy of personal telephone records and the scope of disclosure authorized.

The carriers notices are deficient.� CPNI--Customer Proprietary Network Information--is not a term that consumers understand.� Even when it is defined, CPNI still has no meaning to a reasonable consumer.

The FCC should devote significant attention to the notices that carriers are issuing.� We recommend following the guidance recently issued by the Federal Trade Commission on improving notices in the financial services industry.[25]�

Many CPNI notices do not use the word "privacy," nor do they state in plain language that CPNI refers to their calling records.� These notices also contain language designed to encourage individuals not to take action (e.g. "no action by you is required�").

Take, for instance, this Verizon CPNI notice.� It appeared on the back side of the last page of the bill.� It does not contain the word "privacy."� CPNI is described in a technically-correct, but obtuse fashion: "the type, technical arrangement, quantity, destination, and amount of use of telecommunications services�"

After this notice was issued, callers to the Verizon opt out number encountered a cumbersome and confusing process. To opt out, callers had to have their bill in hand.� Individuals were required to provide their phone number, their account number, the name on the account, their address, and speak the name of the �authorized� person to make decisions on the account. This process places an unreasonable burden on consumers who simply wish to protect their privacy. Further, the script used by Verizon to guide consumers through the opt-out process employs language that discourages individuals from exercising their rights. For instance, when a consumer chooses to opt-out, the script responds, �You are requesting to establish a restriction on your account���a characterization that misleads customers about the ramifications of their decision. These procedures are designed to stop people from opting out.

28. Should the Commission adopt any additional reporting requirements related to the disclosure of CPNI?

We note that upon suggesting that CPNI access was a systemic problem at carriers, CTIA reacted with ad hominem invective instead of addressing the issues raised by the EPIC Petition.� It was only after the problem was so well documented that it was undeniable that we began to witness positive movement on this issue.

The problem, as with many privacy violations, is one of observation.� Privacy violations are often difficult to observe, and once observed, are often explained away as a single incident rather than a pattern.� Reporting and transparency are needed in order to fairly evaluate emerging privacy risks.�

Respectfully Submitted,

Chris Hoofnagle

Electronic Privacy Information Center

West Coast Office

944 Market St. #709

San Francisco, CA 94102

Hoofnagle@epic.org

415-981-6400

Linda Sherry

Director, National Priorities

Consumer Action

Remar Sutton

Co-founder

Privacy Rights now Coalition

Jeff Chester

Executive Director

Center for Digital Democracy

Jean Ann Fox

Director of Consumer Protection

Consumer Federation of America

Robert Ellis Smith

Publisher

Privacy Journal

J . Bradley Jansen

Director

Center for Financial Privacy and Human Rights

Susan Grant

Vice President, Public Policy

National Consumers League

[1] Customer Proprietary Network Information, 71 Fed. Reg. 1317 (Mar. 15, 2006).

[2] Petition of the Electronic Privacy Information Center for Rulemaking to Enhance Security and Authentication Standards for Access to Customer Proprietary Network Information, CC Docket No. 96-115 (filed Aug. 30, 2005) (EPIC Petition).

[3] Bob Sullivan, Study: ID theft usually an inside job; Up to 70 percent of cases start with employee heist, MSNBC, May 21, 2004, available at http://www.msnbc.msn.com/id/5015565/.

[4]Office of the Comptroller of the Currency, Identity Theft: Organized Gang and Teller Collusion Schemes (Apr. 25, 2002), available at http://www.occ.treas.gov/ftp/alert/2002-4.txt.

[5] See Paul M. Schwartz & Joel R. Reidenberg, Data Privacy Law: A Study of United States Data

Protection 329-30 (1996) ("The industry itself recommends the use of only vague notices that do not offer

meaningful disclosure of practices.")

[6] Id. See also Privacy Rights Clearinghouse Second Annual Report 21 (1995), cited in Jerry Kang,

Information Privacy in Cyberspace Transactions, 50 Stan. L. Rev. 1193, 1253 n.255 (1998) (�Many

consumers are unaware of personal information collection and marketing practices. They are misinformed

about the scope of existing privacy law, and generally believe there are far more safeguards than actually

exist.�)

[7] Jane Spencer, What Part of 'Cancel' Don't You Understand? Regulators Crack Down on Internet Providers, Phone Companies That Make It Hard to Quit, Wall Street Journal, Nov. 13, 2003.

[8] Ryan Singel, Acxiom Opts Out of Opt-Out, Wired News, Nov. 17, 2003, available at�

http://www.wired.com/news/privacy/0,1848,61240,00.html

[9] Respectively, at 20 U.S.C. � 1232 g, 47 U.S.C. � 551, 18 U.S.C. � 2510 et. seq., 18 U.S.C. � 2710, 18 U.S.C. � 2721, and 15 U.S.C. � 6501.

[10] Anders Gyllenhaal & Ken Paulson, Freedom of Information in the Digital Age, Apr. 2001, at http://www.freedomforum.org/.

[11] The Privacy Best Practice, Forrester Research, Sept. 1999.

[12] Susannah Fox, Trust and Privacy Online: Why Americans Want to Rewrite the Rules, the Pew Internet & American Life Project, Aug. 20, 2000.

[13] Business Week/Harris Poll: A Growing Threat, BusinessWeek, Mar. 20, 2000, at http://www.businessweek.com:/2000/00_12/b3673010.htm.

[14] See North Dakota Secretary of State, Citizens for North Dakota's Future Year End Measure Report (2002)($193,000 raised); cf. North Dakota Secretary of State, Protect Our Privacy's Year End Measure Report (2002)($27,000 raised).

[15]North Dakota Secretary of State, Official Election Results (Jun. 11, 2002).

[16] See Letter from Marc Rotenberg, Executive Director, Electronic Privacy Information Center, to Ivan Seidenberg, President and co-CEO, Verizon (Feb. 7, 2002), at http://www.epic.org/privacy/cpni/verizonletter.html.

[17] See e.g. http://www.epic.org/privacy/cpni/verizon_optout.jpg.

[18] See Privacy Rights Clearinghouse, Opt Out of Releasing Customer Proprietary Network Information (CPNI), Apr. 2004, http://www.privacyrights.org/fs/fs1aplus-cpni.htm.

[19] "I spent 30 minutes on the phone with T-Mobile customer service (611) recently trying to opt out of CPNI sharing. The person I spoke to had no idea what I was talking about was, even after I explained it in detail. The closest thing she knew of was preventing my name from appearing on Caller ID. Later in the call, after some time spent on hold, she read me a PR statement from T-Mobile commenting on the procuring of call data by unscrupulous companies (T-Mobile doesn't condone it, blah blah) and offered to put a password on my account so this couldn't be done.

"At one point, I explained that the FCC provides for this right of consumers to opt out of CPNI sharing, etc., and she suggested I call the FCC to ask them exactly what this "Customer Proprietary Network Information" is all about -- 'cause she sure never heard of it."� See Adam Shostak, Selling Your Phone Records, Emergent Chaos, Feb. 10, 2006, available at http://www.emergentchaos.com/archives/2006/02/selling_your_ph.html

[20] 182 F.3d 1224 (10th Cir. 1999).

[21] Most recently, in White Buffalo Ventures, LLC v. Univ. of Texas, 420 F.3d 366 (5th Cir. 2005), cert. Denied, 2006 U.S. LEXIS 61 (U.S. Jan. 9, 2006) (Supreme Court denied review of a 5th Circuit decision that rejected a First Amendment challenge to the spam filtering performed at a public university); Trans Union v. FTC, 245 F.3d 809 (D.C. Cir. 2001), rehearing denied, 267 F.3d 1138 (2001), cert. denied, 122 S. Ct. 2386 (U.S. 2002) (D.C. Circuit upheld the Fair Credit Reporting Act against First Amendment challenges to restrictions on marketing use of credit files); Trans Union v. FTC, 295 F.3d 42 (D.C. Cir. 2002), rehearing en banc denied, 2002 U.S. App. LEXIS 22105 (D.C. Cir. Oct. 22, 2002) (D.C. Circuit rejected a First Amendment challenge to the provisions of the Gramm-Leach-Bliley Act prohibiting secondary use of Social Security Numbers).� Many courts have upheld the Telephone Consumer Protection Act, the law that creates the authority for the Do-Not-Call list, opt-in prohibitions on sending junk faxes, and prohibitions on prerecorded phone messages. Most recently, in Missouri ex rel. Nixon v. Am. Blast Fax, Inc., 323 F.3d 649 (8th Cir. 2003), cert. Denied, 540 U.S. 1104 (US 2004), the 8th Circuit upheld it, in yet another case that was denied review by the Supreme Court. Other cases upholding the TCPA against First Amendment attack include: Destination Ventures, Ltd. v. F.C.C., 46 F.3d 54 (9th Cir. 1995); Moser v. FCC, 46 F.3d 970 (9th Cir. 1995) cert. Denied, 515 U.S. 1161 (1995); and there are several district court level decisions upholding the law.� In Anderson v. Treadwell, 294 F.3d 453, (2d Cir. 2002), cert. Denied, 538 U.S. 906 (US 2003), the Second Circuit upheld a New York state "anti-blockbusting" law, one that allowed homeowners to opt-out of solicitations designed to churn the hosing market by highlighting racial influx in the neighborhood. Even the right to force people to receive these distasteful solicitations was appealed to the Supreme Court, but they chose not to take the case.

[22] Mainstream Mktg. Servs. v. FTC, 358 F.3d 1228 (10th Cir 2004), cert. Denied, 125 S. Ct. 47 (US 2004).

[23] Li Yuan, Companies Face System Attacks From Inside, Too, Wall Street Journal, Jun. 1, 2005, available at http://online.wsj.com/article/SB111758346264947645.html.

[24] See http://myfloridalegal.com/webfiles.nsf/WF/MRAY-6M9RY3/$file/Global_Complaint.pdf.

[25] See http://www.ftc.gov/opa/2006/03/jointprprivacy.htm